Many Americans have been sold term life insurance due to its supposed low cost. However, this totally fails to account for the Lost Opportunity Cost (LOC), in other words, what the money spent on term life insurance could accomplish elsewhere.

You’ve all heard the radio ad along the lines of, “I got him 1 million dollars of term insurance for only $200 a month.” It’s in the series of radio ads where the insurance guy finds Big Lou, “who’s just like you except he’s only on number two,” a million dollars of term life insurance “for only $200 per month”. The number two, in the ad, refers to the fact that Lou is only on his second wife. In the series of ads another line talks about Lou acquiring the insurance ‘even though he’s on meds too’ and the insurance is at a price ‘he can live with’. In one of the ads it explains how his new trophy wife wants him to get more life insurance. One ad wraps up with the words. “… to get the savings you deserve on Life Insurance…”

Big Lou is a fictitious character designed to portray an average consumer. Since Lou is to somehow supposed to represent you, it would be wise for you to use Lou’s decision to evaluate the true cost of purchasing term life insurance.

TermProvider would have you believe that the insurance only costs $200 a month. The reality is that the LOC, will actually cost Lou over $3,000/ month, over the course of 26 years, and I will demonstrate it to you below.

Today’s blog focuses on the cost of the term insurance, not the price. Price is defined as the amount of money you pay for goods or services today. We define cost as the amount a financial decision costs over a period of time. When an analysis like this is done it is an economic evaluation and done over the “life of a project”.

In the case of Big Lou, we evaluate the cost over his entire lifetime and his wife’s lifetime. Here are some assumptions: His trophy wife is 37. Because of his diabetes he pays a little more for his term insurance ($200/month). It is only 10 year term however. Why? When someone is driving home a point about price they will quote you the cheapest rate. Big Lou is a brand of TermProvider. SelectQuote does the same thing. Because the insurance is treated like a commodity the key is to get you in the door with the lowest price. Another way of controlling the price you are enticed with is to limit the rate classes you are allowed as a consumer to see. A rate class determines the price of the insurance based on your health. Zander insurance, which is endorsed by Dave Ramsey, will not give you the option of a “rate class” below standard. Why? Perhaps because this would disclose higher prices. When Dave Ramsey quotes term life insurance rates, I have observed, he will utilize superior rating classes which a very small percentage of the population are eligible for. You should ask, what is the motivation for doing this?

10 years into this decision (age 60), Lou finds himself in a situation where his investments did not earn a true 12% each and every year, and he needs to continue the coverage. His planning was based on using a 12% rate of return (ROR) because this is what he was told the stock market has “averaged” over many, many decades. Because of this he determined, for his wife, he must continue the life insurance coverage. When he renews, fortunately, he is still insurable and is able to apply for new insurance instead of letting his existing 10 year term enter the horrendous premium schedule following the initial term period. He is lucky. From age 60 to 65 he only has to pay $530 per month. Remember, Lou is renting this insurance so the cost must go up as he gets older. Please note Big Lou believes he will be “self insured” at his retirement and he will no longer “need” the insurance. This ignores planning techniques incorporating life insurance which could enhance his retirement income and why he may want it.

Now we evaluate the total cost of his financial decision. The first thing we need to establish is what rate of return assumption we want to consider the money could have earned if we were able to keep it in our wealth building world. This is used to determine the compounding impact of the initial lost opportunity cost (LOC). We use 5%. This same 5% LOC needs to be applied consistently to any financial decision compared to the one we are doing.

Put another way, this is the rate of return we assume Big Lou could have earned on his money if he had made another financial decision versus the choice to purchase term insurance to keep his trophy wife happy. Because he has purchased term insurance, unless he dies before the 15 year period expires, which statistically is unlikely, there will not be a death benefit paid out.

For those of you who think you should use 12% as your lost ROR to calculate the impact of LOC’s your situation would look much worse than just assuming you could only earn 5% on all of your money over a long period of time. On the flip side in order to understand the behavior of money and how it impacts your finances you will realize you cannot apply an average rate of return to predict future account values. You must use geometric rate of return assumptions in your planning. Once you do this, and see how you will not end up with as much money as you had expected, you also will then discover that it is not as easy to “cover up” the impact of your financial decisions as easily. Everything will look great if you assume you are going to earn a 12% rate of return every year of your life. I include this thought for the Dave Ramsey fans reading this. It is also important to note that Dave’s advice does not include consideration for LOCs.

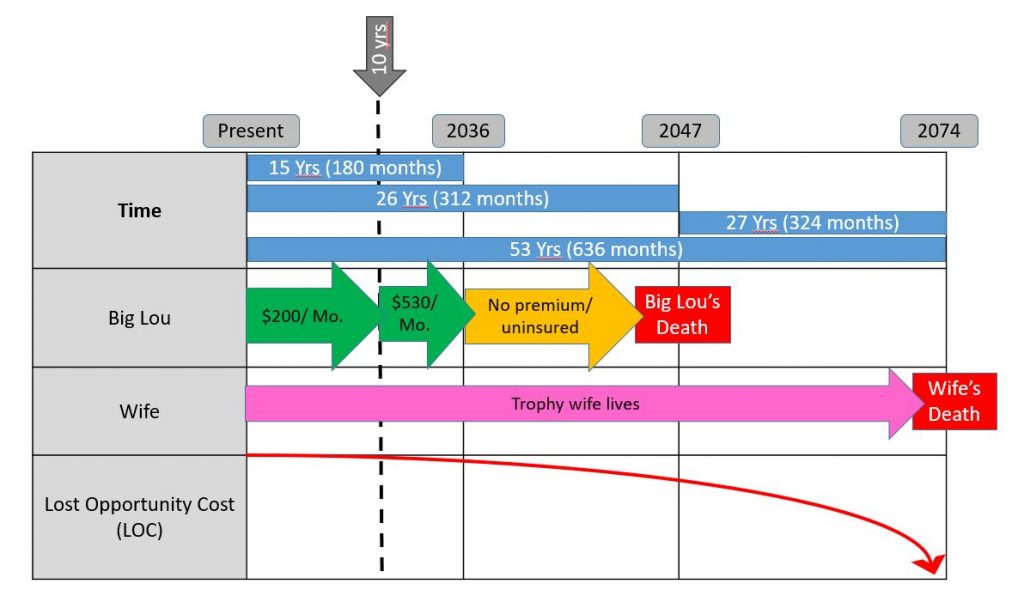

The second thing we must determine is the time period we are going to evaluate. I refer to this as the “life of the project”. This will give us the true cost of Lou’s decision. Most financial planning only evaluates the upside of decisions not the costs of a decision. When finances are evaluated economically, the true cost is subtracted from what the maximum potential of wealth building and its use. We are going to evaluate the true cost of three separate projects. They are the day before Lou dies, the day after his death and the day of the trophy wife’s death. This third evaluation will consider two different potential paths which could be chosen by Lou’s widow.

The follow chronological chart will help decipher time frames. Big Lou will live to age 76 and his trophy wife lives to age 90.

Here are the true costs of Big Lou’s decision:

1. The day before Lou’s death

$55,800 the cost of premiums for 15 years ($200/mo. for 10 years + $530/mo for 5 years)

+ $76,500 – The interest Lou would have earned on the premiums over 26 years

-$7,696 on the $200/mo. for 10 years + this money then growing for 16 years at 5% until Lou’s death $37,492

-$5,100 on the $520/mo. for 5 years + this money then growing for 11 years at 5% until Lou’s death $26,212

= $132,300 – The total lost of premiums paid + lost interest earnings at a 5% rate over the 26 years period.

$132,300 ÷ 312 months (Life of the this project/the day before Lou’s death) = $507/month cost.

I thought the term insurance was only going to cost $200 per month!

2. The day after Lou’s death

$132,300 – The cost of the premiums paid and the interest not earned on that money.

+$1,000,000 – The death benefit which was not paid out.

= $1,132,300 – Total lost opportunity cost over Lou’s life

$1,132,300 ÷ 312 months (life of the project/the day after Lou’s death) = $3,629/month cost.

I thought the term insurance was only going to cost $200 per month!

3. The day of the Trophy Wife’s Death

A. Using a spend down technique for income after Lou’s death.

(In this scenario, the widow would have taken the $1 million dollar death benefit and annuitized it, to pay her a guaranteed lifetime income. This is done with a Single Premium Immediate Annuity (SPIA). This is a spend down technique. At her death the income ends.

$493,936 (At Lou’s death, the true cost of the premium paid was $132,300 If this dollar amount was allowed to grow, assuming the same 5% return, over 27 years (years the widow lives) the dollar amount lost would grow to $493,936 at the widow’s death.

+$1,620,000 (The SPIA is estimated to pay out $60,000 / year for life. Because the widow lives for 27 years after Lou’s death, the total income given up is $1,620,000.

= $2,113,936 = Total lost opportunity cost

$2,113,936 ÷ 636 months (Life of the project) = $3,324 / month cost

I thought the term insurance was only going to cost $200 per month!

or

$2,113,936 ÷ 180 months = $11,744 (This is the true monthly cost of Lou’s decision over the 15 years he paid the premium because of the lost opportunity because of the lost premium, the money those premiums could have earned and the lost guaranteed income, because the death benefit was not paid.)

I thought the term insurance was only going to cost $200 per month!

B. The widow earns 3% per year on the 1 million dollars and uses it for income to live on ($30,000 / year). The $1 million still remains at her demise and is either passed to someone’s children or given to charity.

$493,936 (Principal and interest lost from premiums paid over the 53 years)

+ $810,000 ($30,000 per year times 27 years)

+ $1,000,000 principal which would produce the 3% income which is not passed to the next generation.

= $2,303,936 Total lost opportunity costs

$2,303,936 ÷ 636 months = $3,623 (The cost per month over the life of this project/trophy wife’s life with lifetime using earnings from death benefit which was did not take place.)

I thought the term insurance was only going to cost $200 per month!

or

=$2,303,936 ÷ 180 months = $12,800/mo. (This is the true monthly cost to Lou over the 15 years he paid the premium.)

I thought the term insurance was only going to cost $200 per month!

Remember, in the ad, the person talking said he got Big Lou $1 million of life insurance for only $200 per month. The $200 is merely the price of the premium – it has nothing to do with the true cost of Big Lou’s decision and, for that matter, perhaps yours. Perhaps, you are allowing this sort of influence to control your financial decisions. It is even possible the person offering this type of insurance calls anyone else who offers permanent life insurance scum, but who is telling the truth? Should a person disclosing the truth of a financial decision be called scum?

Your natural tendency is to blow off the reality of financial decisions by assuming you will earn a lot of money through investing. Obviously investments might earn a higher internal ROR than life insurance, but the analysis cannot stop there. To be fair, an economic analysis of buying term life insurance and investing the difference or buying permanent life insurance and investing the different would both need to include a calculation of opportunity costs. Not including the costs in either equation only provides partial truth. One of the key elements is to learn how to use the death benefit in retirement as asset replacement insurance and position yourself to enjoy your assets for lifestyle while you are alive (Not covered here). The death benefit can take care of a survivor. The benefit which the trophy wife was not able to utilize because of Big Lou’s decision created a lost opportunity which came at a price.

An “investment only” approach also adds risk and has all kinds of other issues not discussed here. Perhaps the key is to have some sort of balance between insurance which is owned, and not rented, and a variety of other assets including investments which are coordinated to work together. Permanent life insurance is another asset just like real estate and investments. They each carry benefits and negative aspects. They each involve lost opportunity costs. In this blog, we are not going to evaluate lost opportunity costs of purchasing permanent life insurance or real estate. The point here is to show you how lost opportunity costs exist and should not be ignored. You can chose to ignore them but they still exist and impact you. Perhaps the impact they have is one of the reasons it is so hard to get ahead financially.

It is so sad most ‘financial planning’ misses this consideration and so much emphasis is on rates of return. Perhaps we would all be better off if we evaluated our decisions economically and not evaluated isolated black boxes to make predictions of how much money we ‘are going to have’ in an account.

The following are questions you should be pondering as you think about the material here:

Is price or cost a more important consideration?

– Can Lou’s investments make up for the lost opportunity cost?

– When lost opportunity costs are considered, is it possible we give up more wealth than we are able to accumulate?

Do financial institutions understand what is going on here?

– Could the people pushing the term insurance be taking advantage of us?

– Are we being taken advantage of because price is easier to wrap our heads around than true cost?

– Are insurance companies and the people who push this as the only approach making a lot of money off of us?

Most importantly, what could my term life insurance premium be doing for me?

…Financial Well-Being through Sound Instruction